Rocket Fuel Newsletter – How America’s aging housing supply impacts homeowners

DoorDash and Klarna have struck a deal to allow users to pay for meal deliveries with installment loans. “Eat now, pay later” and “CBOs: Collateralized Burrito Obligations” were common phrases thrown around by those mocking the idea of taking out a loan to pay for a burrito from Chipotle. Despite the jokes, “buy now, pay later” (BNPL) has become a habit of many consumers.

This week consumer confidence hits new lows, home prices and sales trend upward, and we investigate the aging housing supply and how it could impact home improvements.

Fuel up! 🚀

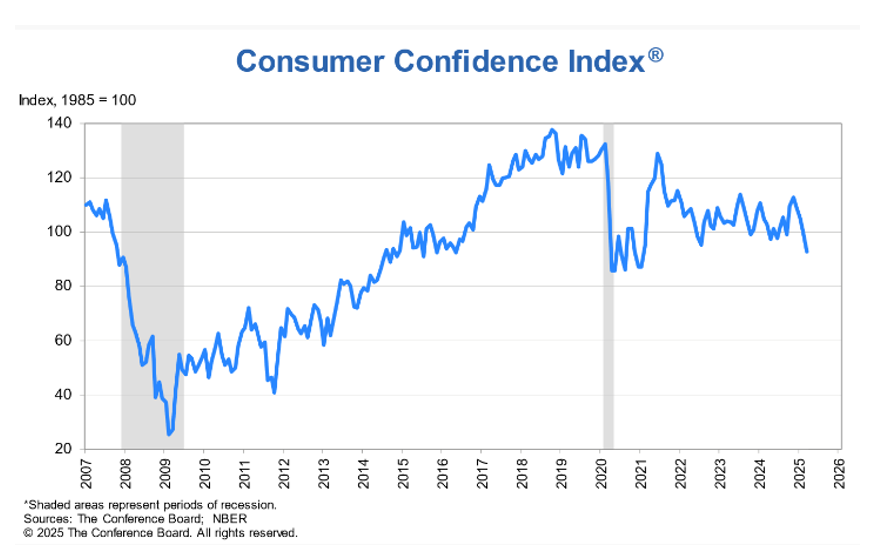

Consumer confidence continues to fall

The Consumer Confidence Index fell by 7.2 points in March to 92.9. This is the fourth consecutive month of declines and the lowest level since 2021.

The Expectations Index, a short-term outlook for income, business, and labor market conditions, hit a 12-year low. Purchasing plans for both homes and cars declined for consumers on a 6-month moving average basis.

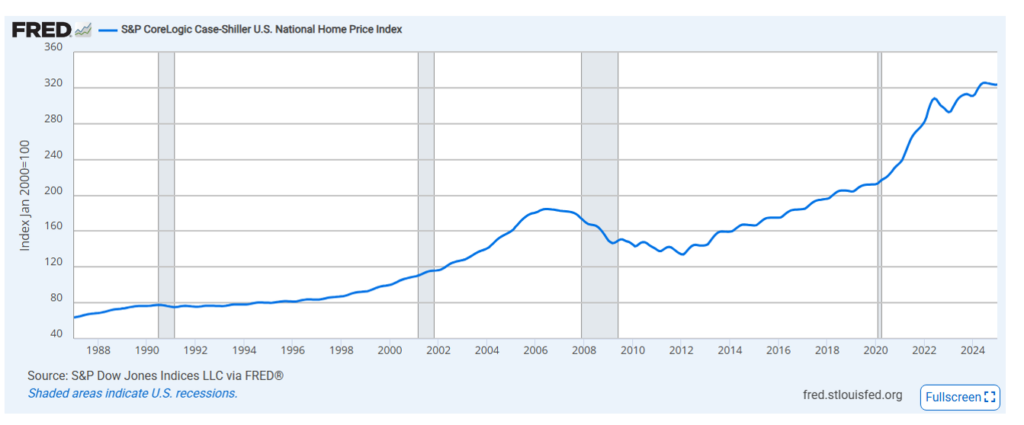

Home prices continue climbing

In January, the Case-Shiller U.S. National Home Price Index rose 4.1% annually and was up from 4% in December. New York and Chicago led the way with 7.5+% increases, while Tampa was the only metro area measured that decreased year over year (-1.51%).

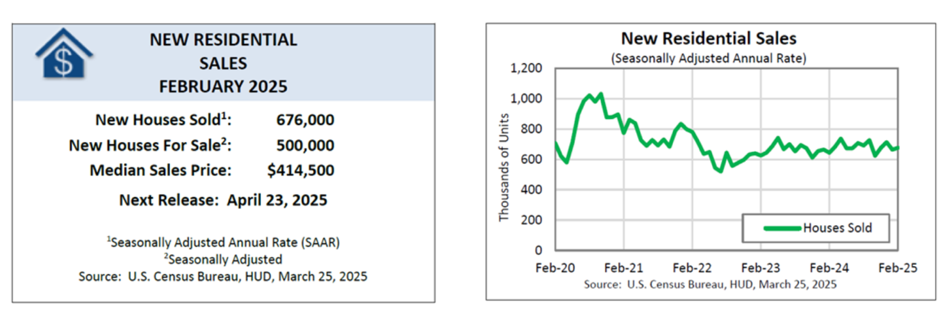

New home sales bounce back after tough winter

Sales of new single-family homes rose to 676,000 for February, up 1.8% from the revised January numbers. The median price of new homes sold in February was $414,500 and at the end of the month there were 500,000 homes on the market, which is close to a 9-month supply based on the pace of sales.

The U.S. housing stock is aging

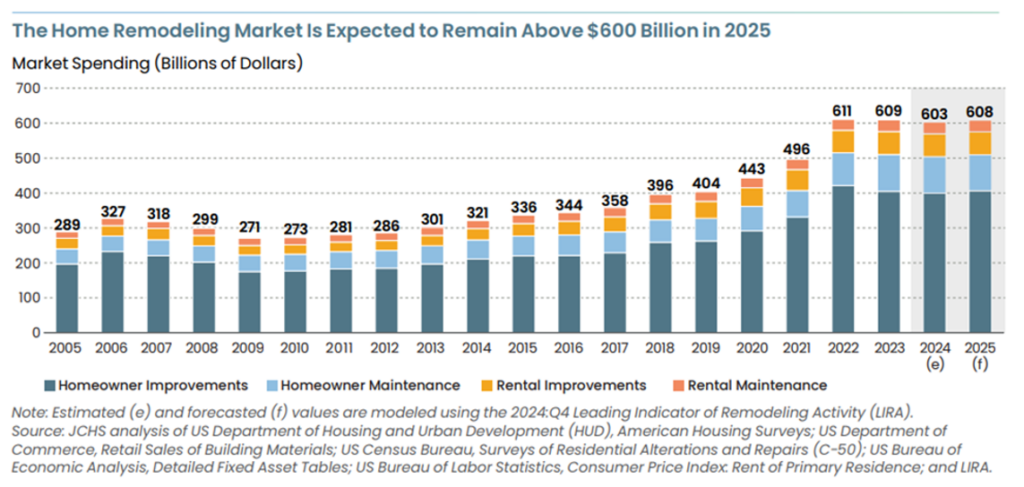

Since the pandemic, home remodeling has taken off. It is estimated to be a $600 billion market in 2025 and has been over $600 billion since 2022. Despite seeing immense growth from 2021 to 2022, remodeling expenses have continued to maintain this growth and don't show many signs of stopping. (Seen in Figure #1).

Figure #1:

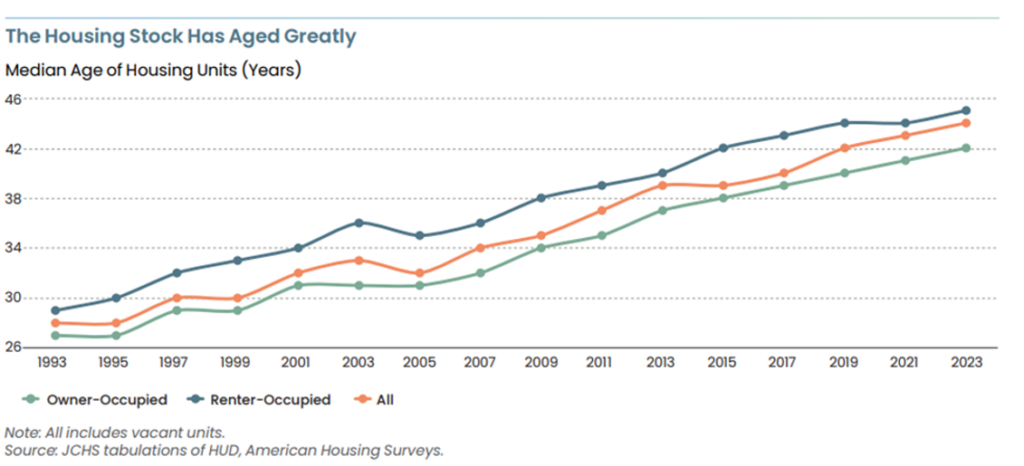

A lot of this can be attributed to the aging homes that are in the United States right now. Despite new home building and completions hitting record highs during the pandemic, overall, the age of the U.S. housing stock has been steadily increasing. The median age of a house is over 42 years (Figure #2).

Figure #2

It is estimated the housing stock age will only increase in the coming years. Owners with older homes spend more money on maintenance and improvements when compared to newer homes (Figure #3). Additionally, energy-related improvements grow progressively more expensive.

Figure #3

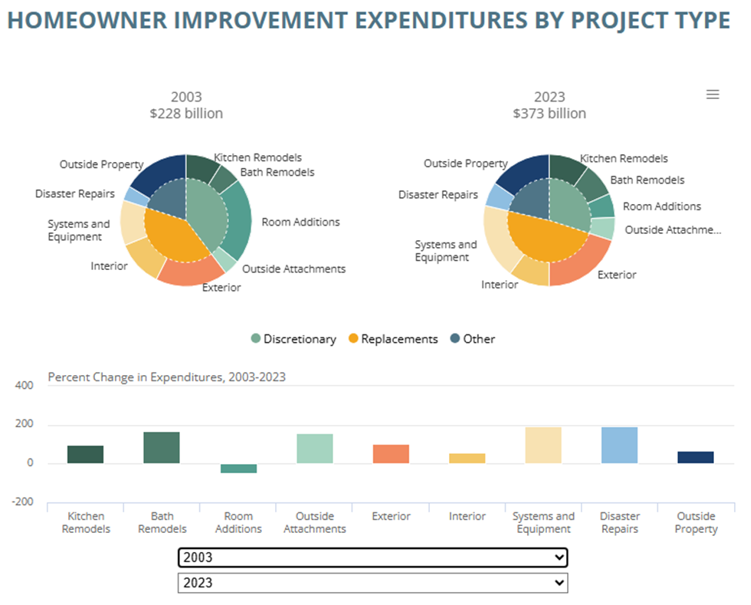

All these changes can easily be seen in how home improvement expenditures have been changing over the last 20 years (Figure #4). As seen in the graphic below, over the past 20 years, more income has had to be allocated to house replacements and disaster repairs in comparison to discretionary spending.

Figure #4

The U.S. homeownership market is undergoing significant changes. The costs associated with maintaining a home are increasing. As the housing landscape evolves, it is critical for individuals and families to know the potential impact of homeownership.

To access the full Joint Center for Housing Studies of Harvard University article, click here.

Purchase season is gearing up. Stay ahead by engaging with industry leaders and discovering what’s next. We’ll be at these top events – let’s connect!

- March 31 – April 2: Live Unreal Lead UP – Miami, FL

- April 23 – 25: Texas Bankers Association Annual Convention - San Antonio, TX

- April 28 – May 1: Consumer & Residential Mortgage Lending Conference – San Antonio, TX

- April 30 – May 2: Farm Credit Home Lending Conference – Long Beach, CA

Join us for meaningful conversations, valuable insights, and new opportunities to drive your business forward. We look forward to seeing you there.

This week’s puzzle gets 5 Rockets out of 5.

Good luck!