Rocket Fuel Newsletter – Home buying trends, climate change impact, and fears of a recession

The Great Gatsby turns 100 years old this month! The timeless classic has been beloved by millions for its depiction of the American Dream, wealth, and love.

This week, selling stocks for a down payment, climate change’s effect on the housing crisis, tiny homes, and how probable stagflation is.

Fuel up! 🚀

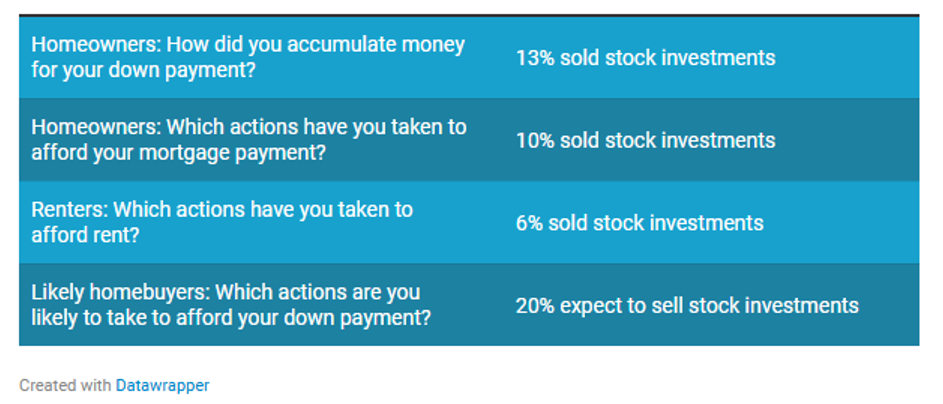

1 in 5 home buyers expect to sell stocks to fund a down payment

The stock market has recently experienced some of its most challenging performances in nearly 5 years, potentially impacting home buying prospects. According to a Redfin survey, approximately 20% of prospective home buyers are considering selling stocks to help fund their down payment.

Access Redfin’s full article here.

Climate change and the U.S. housing crisis

Climate change-related disasters have become frequent, significantly raising the cost of housing repairs in vulnerable areas. This trend is placing substantial stress on insurance markets and their ability to provide comprehensive coverage. As a result, many states are increasingly relying on insurers of last resort, which have been established in high-risk disaster regions to ensure continued housing insurance availability.

Read more about this from Harvard Magazine here.

Tiny homes are a potential solution in LA

Since the LA wildfires, many residents have been displaced from their homes and forced to stay in short-term housing while they wait for their homes to be rebuilt. Accessory dwelling units (ADUs) could be a helpful solution in this situation. They have been gaining popularity recently and are projected to experience a 4.2% increase in the next 5 years. Moreover, ADUs are relatively quick to construct, and some parts of them can even be 3D printed.

Click here for the full story.

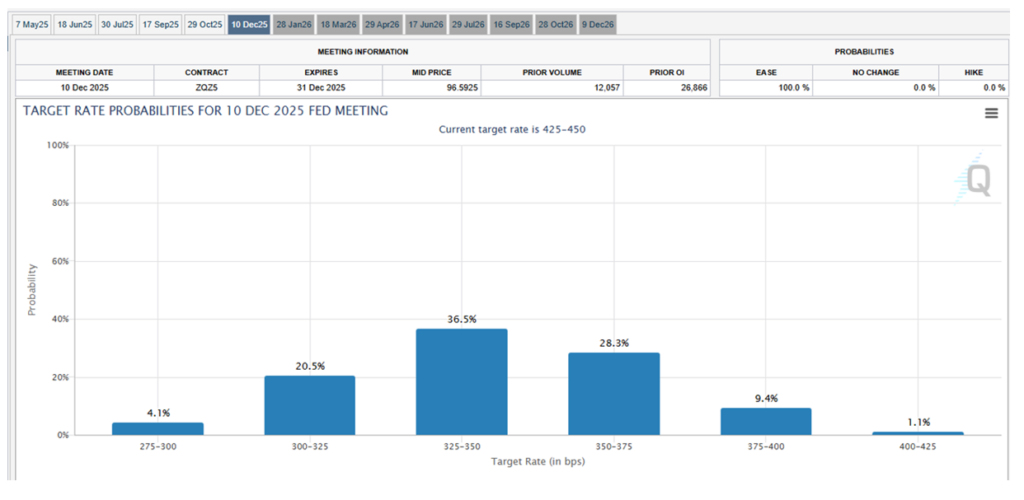

Are we on the verge of stagflation?

Stagflation refers to the highly feared economic condition where high inflation, elevated unemployment, and stagnant growth occur simultaneously. Recent developments have sparked concerns that the U.S. could be headed in that direction.

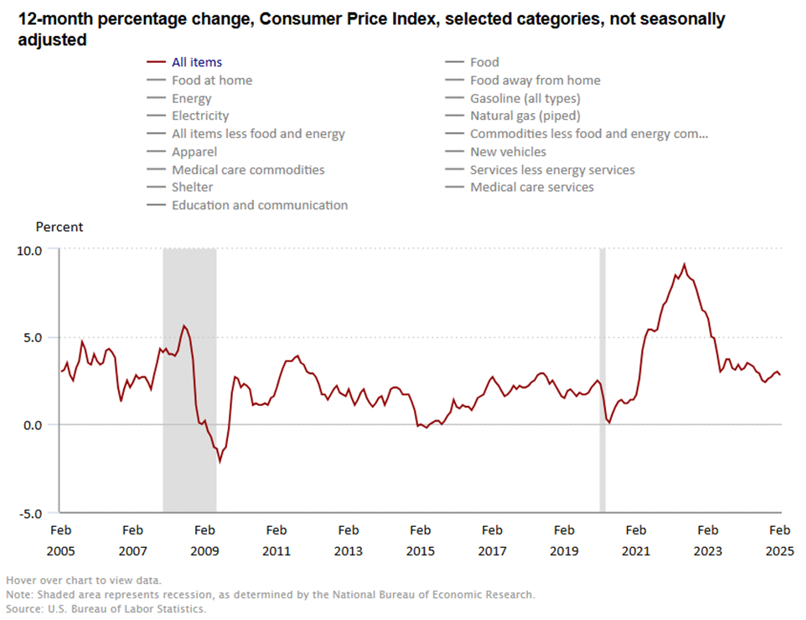

Inflation has been a concern dating back to 2021, and the Federal Reserve has been laser focused on bringing it down to its 2% target. While the recent rate hiking cycle has made meaningful progress, inflation remains above target and has even started to tick back up. The Fed is wary of cutting rates too soon, fearing a resurgence in inflation, and has opted for a cautious “wait and see” approach.

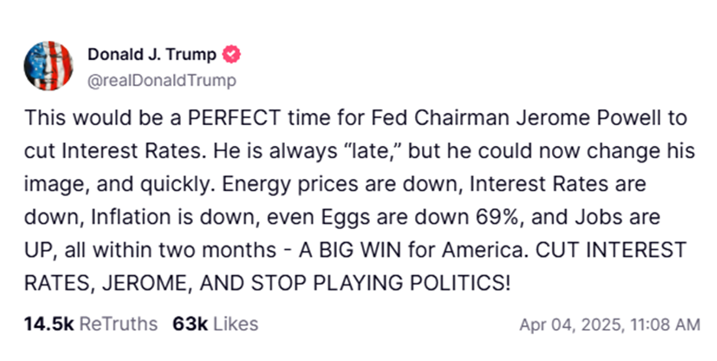

That approach hasn’t sat well with everyone – especially President Trump, who has publicly pushed for immediate rate cuts.

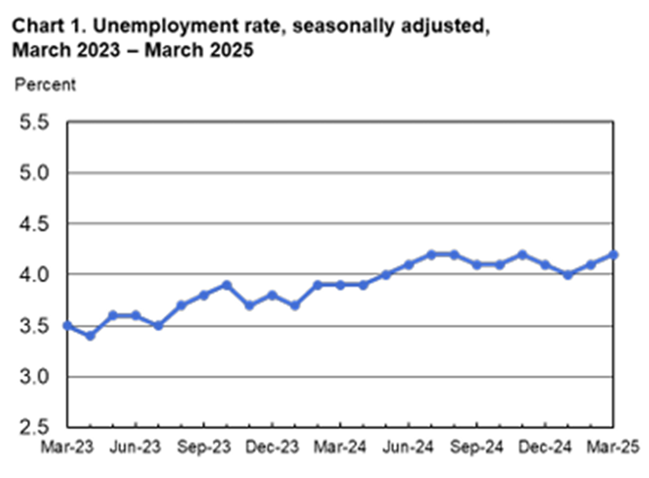

The resilience of the labor market has given the Fed cover to keep rates high and keep its focus solely on reducing inflation, but cracks may be forming. The unemployment rate has been rising gradually and currently sits at 4.2%.

While 4.2% is not concerning, things could change quickly. On April 2, the announcement of sweeping tariffs sent shock waves through financial markets. The tariffs, as they are proposed, are expected to increase consumer prices and production costs, stoking inflation while also threatening economic growth and employment. This puts the Fed – and Chair Jerome Powell – in a tough spot. Powell acknowledged the uncertainty, saying: "We face a highly uncertain outlook with elevated risks of both higher unemployment and higher inflation." Still, he maintained the Fed's position: “We are well positioned to wait for greater clarity before considering any adjustments to our policy stance.”

Markets, however, appear less patient. Traders are now pricing in four rate cuts before the end of the year, signaling growing concern that the economy may be losing steam.

J.P. Morgan (along with many other firms) has been increasing its odds of a recession. After the plan for tariffs was announced, J.P. Morgan sent out a report updating its probability of a recession this year to 60%.

If this trajectory continues, one of the most immediate impacts could be on mortgage rates. In a slowing economy, especially one veering toward recession, yields on long-term bonds tend to fall – bringing mortgage rates down with them. This could offer some relief to prospective home buyers who’ve been sidelined by high borrowing costs. However, if stagflation takes hold – with inflation remaining stubbornly high even as growth slows – mortgage rates may not decline as much as expected or could remain volatile. For now, the housing market remains caught in the crosscurrents of economic uncertainty.

Purchase season is here. Stay prepared by engaging with industry leaders and discovering what’s next. We’ll be at these top events. Let’s connect!

- April 23 – 25: Texas Bankers Association Annual Convention – San Antonio, TX

- April 28 – May 1: Consumer & Residential Mortgage Lending Conference – San Antonio, TX

- April 30 – May 2: Farm Credit Home Lending Conference – Long Beach, CA

- May 8: California Mortgage Expo – Irvine, CA*

*Use the exclusive code ROCKETFREE to waive the registration fee for this event.

Join us for meaningful conversations, valuable insights, and new opportunities to drive your business forward. We look forward to seeing you there.

We’ve had some close calls for puzzle standings in the past – we've even had a few two-way ties. But for the first time in Pro Puzzles history, we had a three-way tie atop the leaderboard! Three solvers finished last week’s puzzle in exactly 55 seconds, outpacing the rest of the field by nearly 20 seconds. Great work!

This week’s puzzle gets 4 Rockets out of 5.

Good luck!