Rocket Fuel Newsletter – 1/06/2025

2024: A 6/10 kind of year?

From reconnecting with loved ones to learning new skills (and maybe even adopting a furry friend), Americans rated this year a solid “meh,” per Talker Research. But hey, personal growth was the real MVP. Compare how 2024 ranks for you and see what made it memorable for others.

This week’s edition explores changes in the rent market, the 2025 Federal Housing Finance Agency (FHFA) scorecard and a look back on 2024.

Fuel up! 🚀

Rent growth slows to post-pandemic lows

The latest CoreLogic report shows single-family rent growth in the U.S. slowing to just 1.7% year-over-year in October 2024 – the lowest since June 2020. Pandemic-driven rental hotspots like Austin and Phoenix are cooling off, with Austin rents down 3% annually.

Meanwhile, markets like Detroit and Washington, D.C., saw the strongest increases at 6% and 4.5%, respectively. This deceleration marks a notable shift after years of steady 2% – 4% growth pre-pandemic.

Read more about CoreLogic’s findings here.

Renters faced record cost burdens in 2023

Slowing rent growth is welcome news, as the Joint Center for Housing Studies of Harvard University recently found that affordability challenges for renters hit an all-time high in 2023. A record 22.6 million households spent over 30% of their income on housing, with lower-income renters dedicating a staggering 80% of their income to rent and utilities.

Even middle- and high-income renters have felt the pinch as rising costs outpaced incomes. With multifamily construction slowing, affordability concerns remain critical.

Dive deeper into the data here.

FHFA 2025 scorecard

The FHFA’s 2025 Scorecard sets ambitious goals for Fannie Mae and Freddie Mac to tackle housing affordability and supply challenges while promoting resilience in the housing market.

Key objectives outlined in the scorecard include improving mortgage process efficiency, supporting sustainable housing outcomes and enhancing risk management frameworks, especially in response to natural disasters and emerging technologies like AI.

Explore the details here.

2024 year in review

Much of 2024 was spent focused on bringing inflation down to the Federal Reserve’s goal of 2%. As we get closer to that goal, progress has somewhat slowed but continues to improve. Personal Consumption Expenditures (PCE), the Fed’s preferred measure of inflation, hit a low of 2.1% back in September and bounced back slightly with the most recent release reporting 2.4% in November.

PCE year-over-year:

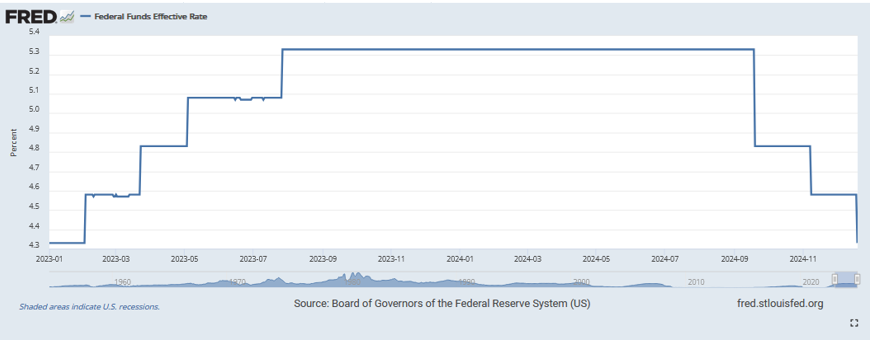

The improved inflation situation has enabled the Federal Reserve to start cutting the federal funds target rate. The first cut was finally made in the September meeting, with a drop of 50 basis points. The lead up to the meeting was met with a dip in mortgage rates, as inflation dropped, and the economy remained relatively healthy in a high-rate environment.

Throughout the year, we continued to hear the same message from the Fed: Expect to see higher rates for longer. The Fed went on to make two additional rate cuts, ending 2024 with a target rate of 4.25% – 4.5%.

FRED federal funds effective rate:

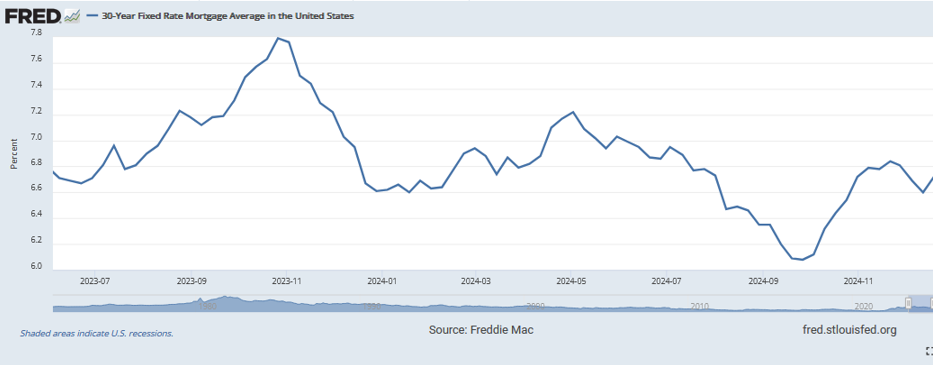

While the federal funds target rate is indirectly tied to mortgage rates, a drop in the former does not always mean a drop in the latter. The mortgage market is always looking toward the future, and with the Federal Reserve continuing to warn of higher rates for longer, the mortgage market seems to be taking that message to heart.

Mortgage rates are more directly tied to the 10-year treasury yield, which can be viewed as a measure of investor sentiment. During times of economic growth, investors often seek riskier investments with higher potential rewards. This means less people are buying bonds, which drives up the bond yield. See the correlation between the two below:

10-year treasury yield:

30-year fixed-rate mortgage:

So, what can we expect to see in 2025? Again, the Federal Reserve has maintained we can expect to see higher (federal funds target) rates for longer. And while this does not directly translate to higher mortgage rates for longer, that is likely the case.

Higher mortgage rates mean we will continue to see higher proportion of purchase mortgages and home equity loans over refinances. Purchases are less sensitive to rates, as home buyers re-locate or make room for growing families.

Start 2025 with us

Chat with us at our upcoming tradeshows. Hear exclusive keynotes from our very own Executive Vice President Mike Fawaz and Vice President Don Chiesa at the New England Mortgage Expo.

Use code ROCKETFREE for free registration at these shows:

- January 15-17: New England Mortgage Expo – Mohegan Sun, CT

- February 11: California Mortgage Expo – Palm Springs, CA

- February 16-18:1 Conference for Community Bankers; Phoenix, AZ

- February 18: Texas Mortgage Roundup – Austin, TX

- February 25: California Mortgage Expo – Sacramento, CA

1Code ROCKETFREE is not eligible for the February 16-18: Conference for Community Bankers – Phoenix, AZ.

Don’t miss your chance to connect. Secure your spot today.

Tough puzzle last week! Our fastest solver finished in 1:33, narrowly defeating second place’s time of 1:39.

This week’s puzzle gets 2 Rockets out of 5.

Good luck!